AI Can Be Your Next Financial Guru

Artificial intelligence is a branch of computer science that makes computers smart enough to take over human jobs. The most common use of AI is in self-driving cars, which are already being tested by Google, Uber, and Tesla.

But AI is no longer just for the future. In fact, the technology is already here, and it’s already being used in the financial services industry.

While there are many areas where AI is already being used, its most common use in financial services is in services that provide financial advice. For example, the company Wealthfront uses AI to create portfolios for its clients, while Betterment uses AI to create investment portfolios and manage clients’ money.

These companies are able to use AI to provide financial advice to their clients because they’re using computers to make the same kind of decisions that human financial advisors would make. So, if you’re interested in speaking with an AI financial advisor, you should know a few things about the technology.

What Does AI Mean for the Future of Finance?

Artificial intelligence is all about making computers learn and become more like humans. Today, AI is used to make computers more like humans in fields like medicine, astronomy, and even the military, but it’s also being used to make financial services smarter.

For example, the artificial intelligence used by LinkedIn to make recommendations to you is being used by the online personal finance company Upstart to make recommendations about who you should lend money to.

While it’s easy to see AI’s potential in fields like medicine, where AI can be used to make sure doctors aren’t missing anything when they diagnose a patient, it’s also being used by financial service companies to make sure clients are making the right decisions about their money.

Because AI is being used to make decisions about how to invest money and how to make money, it’s important to know how exactly these computers are making their decisions.

How Are AI Computers Making Their Decisions?

The goal of AI is to make computers make decisions that are as good as, or better than, the decisions humans make. In addition to being able to learn, one of the ways AI is able to do that is through machine learning.

Essentially, machine learning is a way of getting the computer to learn from its mistakes. For example, if you’re playing a simple game on a computer and the computer makes a mistake, the computer can learn from its mistake and try to make the same mistake less often in the future.

Similarly, if you’re using an online personal finance application to make investment or personal finance decisions, the machine learning will use your mistakes to learn what you should do in the future.

While machine learning is a good way to make computers learn, it’s probably not the only way. Other methods include deep learning, which is when computers are able to figure out how to make decisions on their own, and neural networks, which are basically a way of making computers make decisions like a human would.

Unfortunately, we don’t know exactly how these computers are making their decisions, but we do know that it’s a good idea to pay attention to how the computer is making its decisions.

How Can You Know the Computer Is Making the Right Decisions?

When you use an AI financial advisor to make investment or personal finance decisions for you, you’re basically trusting the computer to make the right decisions. And if the computer is making decisions like a human would, that’s great.

But if the computer is making decisions that are against the advice of human financial advisors, then it’s time to be concerned about how the computer is making its decisions.

For example, most financial advisors would tell you to invest in a diversified portfolio, but a computer might tell you to invest in a single stock. While it’s possible that the single stock will do better than the market, there’s also a chance that the computer’s investment will do worse than the market, or even lose you all your money.

So, if you’re using an AI financial advisor, you should make sure that the computer is making the same types of decisions human financial advisors would make.

For example, you should make sure the computer is recommending a diversified portfolio, which means that you can invest in a mix of stocks, bonds, and other investment vehicles in a way that balances risk and reward.

If the computer is making decisions that are against the advice of human financial advisors, then you might have a problem. In fact, if the computer is making decisions that human financial advisors would never make, you should probably stop using it.

While you might be concerned about the computer making decisions that are against human advice, you have to remember that the computer is still a computer.

For example, if you’re using an AI financial advisor, you should never use it to make decisions that are against human advice. That means that if a computer tells you to invest in a single stock, then you should probably be concerned.

After all, what if the single stock you invest in does badly? Then you might lose all of your money, just because the computer told you to invest in it.

In short, you want to make sure that the computer is making the right decisions for you, but you also don’t want the computer to make decisions that are against human advice. After all, the whole point of using a financial advisor is to make sure you’re making the right decisions.

How Does AI Affect My Financial Future?

While it’s easy to see how AI has already affected the financial services industry, it’s also easy to see how AI will affect it in the future.

Most of the time, AI is used to make decisions. For example, AI is used to make decisions about the investments you should make, which means that it’s actually creating those investments for you.

That means the AI is helping some companies create a product that they’re selling to you. That means that AI is affecting you, because it’s using a product that’s being sold to you.

But, while AI is being used to create financial products, it’s also being used to make financial products for other companies. For example, AI is being used to make financial products for insurance companies, and it’s also being used to make financial products for banks.

This means that the AI is being used to make financial products that are sold to you, as well as financial products that are sold to other companies. But, while that might seem like AI is affecting more than just you, it actually affects you more.

After all, you’re the person who makes the decision of whether or not to use an AI financial advisor. You’re the one who decides to invest in a specific stock or opt for a particular type of insurance.

But, while AI might be affecting you more than other companies, it also affects other companies. For example, an insurance company might choose to use AI to make its insurance products, so you can be sure that AI is affecting that company.

But, even though AI is affecting more than just you, it’s still a good idea to know how AI affects you.

Impacting on the individual

Financial literacy is not something that comes naturally to a lot of people. In India, a 2019 survey by Scripbox—an online mutual funds platform—found that 72 per cent of Indians were unaware of how much money they were to put aside or invest; 56 per cent of the respondents said they lacked the knowledge to handle personal finances effectively. With fears of bankruptcy, rising costs of colleges, goals of financial freedom increasing in most parts of the world, it is imperative that individuals manage their money well. Today, with the skyrocketing employment of technology and digitisation, there appears to be a new approach to tackle this challenge of financial illiteracy: Artificial Intelligence.

Today, machine learning can help with multiple facets of personal finance, ranging from algorithms that guide individuals to make better personal financial decisions to make cash transfers more effortless than ever. It has also been pivotal in facilitating FinTech, a collaborative industry between technology and finance, algorithms to make financial planning and literacy more accessible.

Furthermore, machine learning frameworks are capable of effectively tracking fraudulent transactions, making payments systems safer for users. For example, Razorpay’s solutions enable corporates and other individual users to use most payment access modes such as JioMoney, MobiKwik, Airtel Money, Ola Money, credit and debit cards, UPI, and net banking. Harshil Mathur, Razorpay’s CEO, said in an interview with the Economic Times last year that employing machine learning and AI allowed the company to provide a better customer experience, higher payment success rates and allowed them to make Razorpay safer by issuing transaction limits and having the AI monitor online behaviours—for example, a fraudster would perhaps not spend as much time checking shopping details as a typical shopper would. One can see another instance of this with the Chinese financial services firm Ping An which applied AI for loan applications. The service would ask applicants to answer a series of questions and use facial recognition technology to discern whether the applicant is lying.

Even credit card companies often use ML algorithms to find anomalies in transactions, which can help track down fraudulent transactions. AI, in this case, could link transactions made in two different countries, say Japan and India, to a third transaction made at, say, Tokyo’s airport and decide that the transaction is an honest one. Otherwise, it would trace it as an anomaly and alert the user. Such uses of AI help make online financial platforms safer, thus encouraging more people to benefit from them.

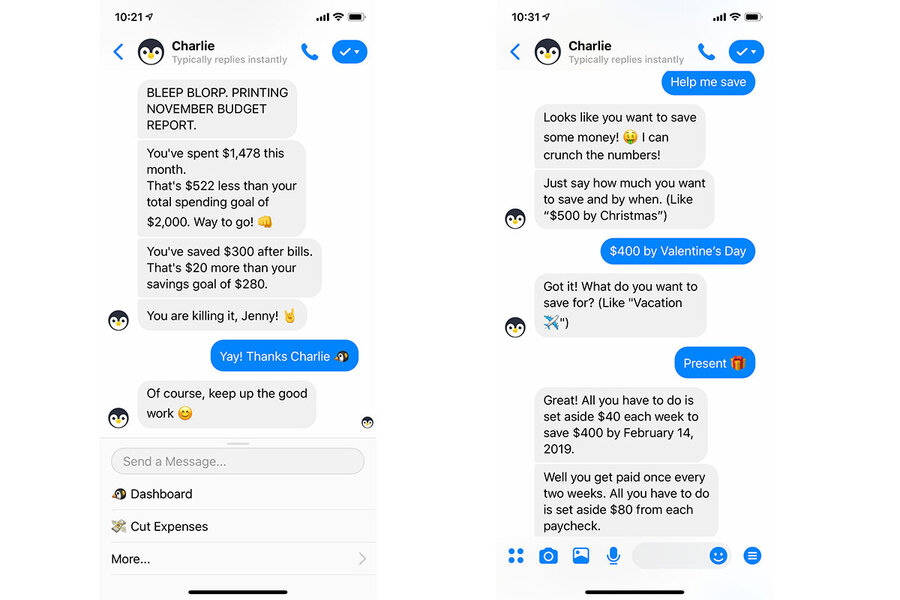

Individuals can also employ AI to make decisions in budgeting and stock trading. One can find apps that help them tackle their debts. Charlie is one such AI-driven budgeting app that began as a chatbot. The American app analyses daily transactions and gives people advice as a bot posing as a cute penguin at the moment. It also flags transactions that go beyond decided limits and allows for certain flexibility in certain expenses, e.g. a daily cup of coffee.

Whereas, Wizely is an Indian alternative to a financial savings app. It also uses AI and ML algorithms, which it uses to give catered financial recommendations to users and allows them to take a ‘financial wellness test’ to get a personalised financial plan of action.

Cleo is another AI-powered Messenger based financial assistant that allows users to manage their finances. allows users to link their bank accounts and send money to Facebook Messenger contacts. Cleo allows users to keep track of savings by allowing them to either manually select a particular amount as savings, or autosave—where Cleo’s AI sees how much someone can save in a week and adds that amount to their Cleo wallet (unless they refuse to do so). Finally, one can also ask Cleo for budgeting advice or whether they can afford to purchase something, and can even expect the AI to roast them if they do not stick to their routine.

The future of financial advising

We can already see AI tools foraying into stock markets. Many AI-powered tools, such as Kavout and Blackbox Stocks, are available today to help make trading in stocks easier for people. These platforms use ML and AI-powered algorithms to look for news and other online data—which they can crunch quickly—to generate insights on stock predictions, strategies and provide analyses on portfolios and markets. Today, many hedge fund managers and brokers use these tools for their work.

So, with its myriad of capabilities, could AI replace financial advisers? Despite the many advancements AI has made in personal finance, the likelihood of AI completely taking over seems low. For one, privacy is an often-cited concern many people have with handing over personal data to AI-powered applications–especially when it comes to technologies such as facial recognition.

Secondly, ML algorithms still fall short of outclassing traditional methods when it comes to time-series modeling. We cannot hard code uncertainties of the real world. At least not yet. A human advisor could also act on the spot and be innovative with their plans, unlike a machine that would stick to standard rules. At the same time, integrating AI tools can reduce human errors and biases. The AI tools mentioned above can definitely encourage financial literacy and enhance financial advisors’ work. In such a world, an individual would be able to use their budgeting apps, transfer money to their parents via messengers, and then go on to financial advisors who can effectively use ML algorithms to better their insights and strategies. Therefore, while completely automated financial advising seems unlikely, many people and firms have welcomed automation in various aspects of financial planning, signalling that AI in financial services is here to stay.

Staff writer. Jonas has an extensive background in AI, Jonas covers cloud computing, big data, and distributed computing. He is also interested in the intersection of these areas with security and privacy. As an ardent gamer reporting on the latest cross platform innovations and releases comes as second nature.